Your Transition

You've been looking forward to retirement for most of your working life. Maybe you've been anticipating relaxing on a beach, traveling, or writing a book. You might have great plans for your retirement, but do you have a financial plan that makes it all possible?

Planning for retirement is about planning beyond your last paycheck.

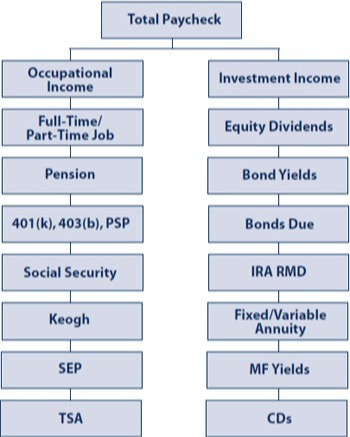

Just because you no longer earn an annual salary does not mean that you have no monthly income. Instead of counting on your job for money, you will rely on two unrelated income streams: investment income and occupational income.

Occupational income

includes any of the following categories: income you continue to earn in a full-time or part-time job; your pension; a 401(k) or 403(b) plan; a profit-sharing plan; social security payments; a Keogh, SEP, SIMPLE, or TSA; or rental income.

Investment income

is comprised of dividends from equities, bond yields, bonds due, mutual fund yields, IRA required minimum distributions, income from a fixed or variable annuity, CDs, and sale of securities.

The key to a successful retirement is the ability to manage wealth after your last paycheck. Our income planning and distribution analysis help us develop a financial plan designed to last you a lifetime. The only plans you need to think about are how to best relax.